The Internal Revenue Service recently issued the 2019 optional standard mileage rates used to calculate the deductible costs of operating an automobile for business, charitable, medical or moving purposes.

Beginning on Jan. 1, 2019, the standard mileage rates for the use of a car (also vans, pickups or panel trucks) will be:

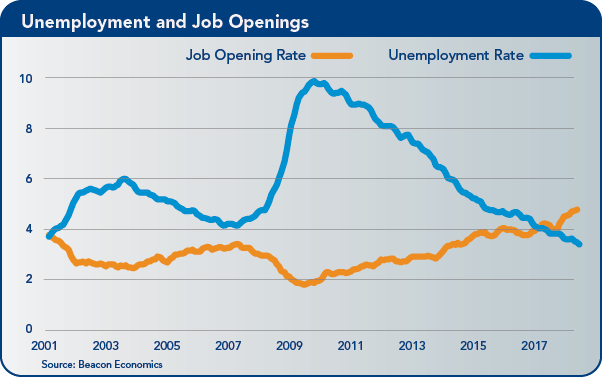

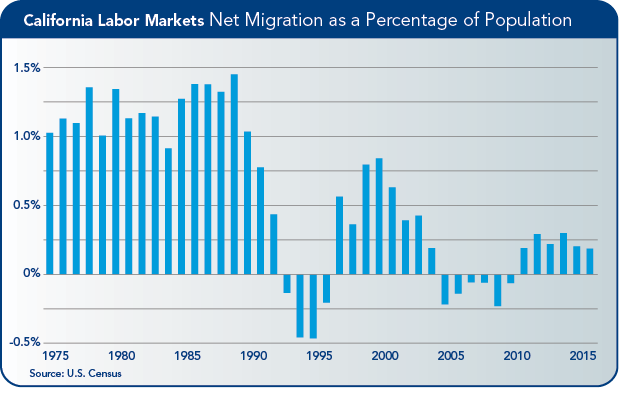

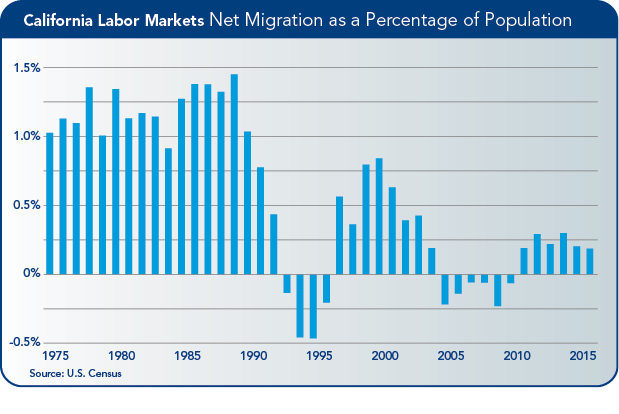

The standard mileage rate for business use is based on an annual study of the fixed and variable costs of operating an automobile. The rate for medical and moving purposes is based on the variable costs. The outlook for the U.S. economy hasn’t changed much over the course of 2018, despite the fact that the nation is on the edge of the longest economic expansion in the nation’s history. Growth has progressed at a steady, sustainable pace since the 2015 commodity bust and mild economic slowdown that occurred that year, according to a recent report by the California Chamber of Commerce Economic Advisory Council. Growth in the last quarter of this year is expected to come in at slightly less than 3%, with growth for the entire year reaching 3.2%. This modest jump is being driven by the fiscal stimulus plan passed by Congress at the end of 2017. Outside of the rapidly growing federal budget deficit, the U.S. economy looks to be well-balanced in terms of the structure of growth with solid fundamentals including private sector debt levels, consumer savings rates, rising wages, the overall pace of homebuilding, and business investment. Unemployment is low—but job growth remains steady. In short, Beacon Economics’ forecast remains boringly positive, and yes, that outlook is expected to stay in place though 2020. This isn’t optimism. Rather, we don’t have any real reason to think otherwise. Read the full report or download PDF. Below are some of the highlights from the economic report. U.S. Trade Policy The only major short-term worry has been wrapped around the direction of U.S. trade policy, but the worst scenarios have not materialized. Rather than unilaterally pull out of the North American Free Trade Agreement (NAFTA) as threatened, the United States instead negotiated a new trade agreement with our two neighbors and largest trading partners that, thankfully, looks almost exactly like the old trade agreement. A brewing trade fight with the European Union that began with steel tariffs also has settled down, and there are now discussions about renewing talks and working toward a new trade agreement. It sounds a lot like T-TIP (Transatlantic Trade and Investment Partnership)—the EU-U.S. trade negotiations canceled by President Trump in one of his first acts in office—although this one will likely be better. Yes, the China trade dispute is still brewing. But even a major trade war with China would not be sufficient to end the current economic expansion. The United States exports fairly little to China—only 8% of all the nation’s exports. And what does get shipped out typically doesn’t have a long supply chain. The greater threat comes from the fact that the United States sources 20% of its manufactured imports from China. But the tariff-increased costs to U.S. importers have been largely offset by a 13% depreciation in the yuan relative to the U.S. dollar. And even as this article is being penned, there are reports, albeit few specifics, of a possible breakthrough in negotiations. Data vs. Discourse All said, from a technical or data standpoint there is not much change in Beacon Economics’ forecast for the U.S. economy. The framing of the outlook is another story. While little has changed in the actual economy, much of the public discourse surrounding the economy has taken a sharp turn for the worse. This new wave of pessimism has likely been driven by the sell-off in the stock market, slowing home sales, and rising interest rates. Yet, as we see it, these short-run trends do not amount to anything that could truly threaten the current expansion. Inflation Worries One wrongly assumed reason for rising rates is inflation. After years of inflation tracking below the Fed-targeted pace, price growth finally increased above the 2% mark. This should have made investors more confident as deflation is less of a risk. Instead, it created a panic about the potential for further increases. Investors need not have worried: the most recent numbers now show inflation back below the 2% range. Beacon Economics expects inflation to remain weak over the next few years. Oil prices are once again down based on high levels of U.S. output. Money supply growth also is very constrained at the moment. And yes, unemployment sits at an extremely low 3.7%—but if this were going to have an effect, we would already feel inflationary pressures on the economy. Housing The U.S. housing market has slowed as a result of the bump in mortgage rates, which has created considerable consternation. However, there is a big difference between a housing pause and a housing bust. The U.S. housing market is not overpriced, nor has there been much risky lending—or lending in general—occurring. So, for now, Beacon Economics is forecasting the expansion to continue and, barring some unexpected external impact, does not anticipate any major change in economic growth leading up to the 2020 election… for better or worse. California Outlook: Growth Prospects for 2019 As 2018 progressed, it became evident that the California economy would continue to prosper despite the challenge of a tight labor market and concerns about the state’s housing situation. Indeed, California’s economic performance was remarkably steady in 2018, fueled by expansion in the state’s industries, increases in incomes and wages, and in response to federal tax cuts enacted early in the year. Beacon Economics expects a continuation of these trends in 2019 and possibly into 2020.  Job Gains For the month of October, California’s 308,700 year-to-year job gain was the second largest among the 50 states. One-fifth of the increase occurred in Health Care (63,100), followed by Professional, Scientific and Technical Services, Leisure and Hospitality, Administrative Services, Government and Construction, and Transportation. Most headline economic numbers for the state show that California maintained an edge over the nation throughout the year. Its 1.8% yearly growth rate in jobs surpassed the 1.6% gain for the United States in October. California’s gross state product growth outpaced U.S. gross domestic product (GDP) in the second quarter, with a 3.3% year-to-year gain compared to 2.9% nationally. The scant increase in the state’s workforce is cause for concern in 2019, although there is evidence that metro area labor force dynamics are such that rapidly growing regions continue to attract workers, most notably in the San Francisco Bay Area and the Inland Empire.  Growth Industries Looking ahead to 2019, the question is, where will growth occur in California? The answer depends on the type of growth. Over the last three years, half of the job gains among the state’s industries have occurred in its population-serving sectors. This trend was led by Health Care, which accounted for 22% of California’s job gains over the three-year period from 2015 through 2018, followed by Leisure and Hospitality, and Government, and will continue through 2019. Smaller but noteworthy contributions also came from the state’s leading external-facing industries, such as Professional Scientific and Technical Services (9%) and Transportation Services (9%). Combine this with the 11% contribution from Professional, Scientific and Technical Services, and about half of all output generated in California came from tech-related activities over the last three years. Other external industries that weighed in with sizable contributions included Manufacturing at 7% and Transportation at 5%. Among those industries that contributed the largest job gains, only Health Care made a sizable contribution to output at 9% of the total.  Increasing Economic Pie

These findings provide insight into the future direction of the state economy. California can count on increases in employment among its population-serving industries in the coming quarters, but if the state wants to increase the size of the economic pie, it must look to its external industries to fuel that growth. That is the challenge that lies ahead for California’s newly elected governor and the rest of the state. At its December 6 meeting, the Oxnard Chamber of Commerce Board of Directors elected the 2019 Officers. Most of the faces will be quite familiar, as there wasn't much change from the later part of 2018.

Members may recall we had changes in officers mid-year in 2018 due to the relocation of the Board chair. Chair-Elect Stacy Miller stepped up to fill the vacancy at the end of April, and has agreed to stay in that position through 2019. Stacy is the principal of Stacy Miller Public Affairs. Serving as Chair-Elect in 2019 is Celina Zacarias. Celina is the Senior Director of Community and Government Relations at California State University Channel Islands. Celina is very active with a number of other chambers of commerce, so we feel very lucky to have her as Chair-Elect. Amy Fonzo has agreed to serve another year as the Chamber's Immediate Past Chair. Amy is the Manager of External Relations for California Resources Corporation, the largest producer of oil and gas in California. Andrew Kiefer will remain in his position as Vice Chair / Treasurer, where he has served for the past two years. Andrew is the Managing Director for CBIZ MHM, LLC in Oxnard. His firm provides accounting and other services to help businesses grow. New to the slate of Officers in 2019 is Craig Classen. Craig is Regional Vice President for Jani Tek Cleaning Solutions. Craig is active on the Chamber Ambassadors Committee and a graduate of the Oxnard Leadership program. The Officers of the Oxnard Chamber make up its Executive Committee.  CEO, Nancy Lindholm CEO, Nancy Lindholm Message from our CEO - Nancy Lindholm NOTE: We ran this article in the Business Voice last month, but many businesspeople are still not aware of the change coming in electricity suppliers and costs, so we are publishing it again in December. Business people are normally very busy operating their companies, not watching city council meetings to find out how much electricity is going to cost them next year. The city of Oxnard has joined the Clean Power Alliance (CPA), which is a community choice aggregation program. It basically means the city has opted to purchase electricity through the CPA versus investor-owned utilities (such a Southern California Edison). Although Edison will still be delivering power through its grid and billing customers, the power rates will be established by the CPA. In addition to joining the CPA, the Oxnard city council also opted to purchase 100% renewable sources of energy. This is the most expensive type of electricity. The higher rates will be applied to all Oxnard customers – residential and commercial – UNLESS THEY OPT OUT of the 100% renewable rate tier. The city council received a presentation on October 23 covering three different rate tiers to choose from – 36% renewable, 50% renewable, or 100% renewable. Although city staff recommended they select the 50% renewable tier, the council voted for the pricier 100% option. It is estimated the increase in rates will be 7% to 9% higher. Again, customers can OPT OUT of these higher rates. The CPA will be mailing two notifications to customers. If the customers do not respond, they will be paying the 100% renewable rate. Customers can not only OPT OUT of the higher tier rate, but they can OPT OUT of the entire CPA and stay with Edison. However, they must act or they are automatically in the program the city selected. The target implementation dates are February 1, 2019 for residential customers (who will also receive two notifications) and May 1, 2019 for nonresidential customers. So, watch your mail at home and at work to make sure you know what you will be paying for!  The Internal Revenue Service (IRS) recently announced that it is extending the due date for certain 2018 Affordable Care Act (ACA) reporting forms to be provided to employees.

In addition, the IRS notice extends “good faith transition relief” for one more year. The IRS will not penalize employers for incorrect or incomplete forms if they can show that they have made “good-faith efforts” to comply with the information-reporting requirements. According to the IRS, the relief applies to missing and inaccurate taxpayer identification numbers and dates of birth, as well as other information required on the return or statement. No relief is provided if the employer did not timely file or furnish the reports by the applicable deadlines or did not make a good-faith effort to comply. For more information, visit the IRS website.  Stacy Miller Stacy Miller The Oxnard Chamber of Commerce is pleased to share a number of great accomplishments for 2018 that reflect a strong and growing business community.

This year, we celebrated 110 years of service to the Oxnard business community. While business has changed dramatically over the last century-plus, your Chamber’s commitment to helping businesses thrive in Oxnard remains steadfast. With a mighty membership of 478, this year saw an increase of 71 new members—that’s an 11% increase over last year. 319 members choose to renew their membership, reflecting a 5% increase over last year. The Chamber’s Business Voice newsletter is emailed to every member and this year, there were 48 issues including a new addition to the newsletter, "5 Things" we did for business in the past week. The Oxnard Chamber values education that is strategic for its members and this year, we hosted seven knowledge and networking luncheons, including two candidates’ forums, as well as 10 educational sessions of the Oxnard Leadership program. The Chamber’s “Oxnard Young Professionals” group reached 35 members. This is definitely an area we are seeking to grow in the years ahead. The Chamber PAC (Political Action Committee) held a successful fundraiser aboard the Scarlett Belle and was instrumental in 5 of the 7 Chamber-endorsed candidates being elected or re-elected in November. The Chamber celebrated new businesses locating to Oxnard by co-hosting 13 ribbon cutting and groundbreaking ceremonies throughout the year. Helping members get to know one another and encouraging more business to business relationships is vital to growing businesses and this year, the Chamber hosted 10 happy hour mixers and four new member mingle receptions. I hope that you find your Oxnard Chamber of Commerce membership valuable and were able to participate in at least one of these great successes. If you didn’t participate in any of these events or programs, know that the Oxnard Chamber is still working for your business through its strong advocacy programs. We encourage you to get engaged because 2019 promises to be even better! Thank you for your support of the Oxnard Chamber of Commerce. On behalf of the Board of Directors and staff, we wish you and hour family a joyous holiday season. Stacy  Eclipse Water Sports is a mobile business. They exclusively rent Hobie Mirage Eclipse pedal boards, a product like no other water sports product. It is extremely difficult to find facilities that rent them. These pedal boards are wider than traditional paddle boards. Customers find them very easy to balance. Within 5-10 minutes they become an expert.

Visitors to Oxnard can enhance their vacation year-round with this totally unique California experience. It is great exercise and great fun. They guarantee customers will have a wonderful time. The Hobie Mirage Eclipse makes it so simple to just step off the shore and onto the water. Their most popular service is 30 min for $20 during the Winter Season. They also offer longer intervals: 60min, 90min, and 2 hours. Still need convincing? The Hobie Mirage pedal board burns 100s of calories an hour. Your entire body is engaged in the activity. Just step right on and start pedaling. Need to reduce stress? Find your center. Effortlessly pedal. Carve through the water. Every session dissolves stress and improves mental health. Bored of the same routine? Explore your favorite locations in an entirely new way. Surround yourself with nature. Pedal further. Go Faster. Now you will be able to explore the entire Channel Islands Harbor in less time. Come out and try it. Create wonderful memories with your friends and family. For more information visit their website at www.eclipsewatersports.com Email them at eclipsewatersports@gmail.com or call them at (805) 312-2985 California employers that don’t already offer a workplace retirement savings vehicle will be required to either begin offering one via the private market or provide their employees access to CalSavers, a state-run retirement savings plan, as early as June 2020.

The CalSavers pilot program is open for employers to enroll; however, mandatory enrollment and contributions do not go into effect until 2020. Employers need not register until then, or later for smaller employers. Emergency regulations governing the CalSavers program were recently approved by the Office of Administrative Law. CalSavers is the result of 2016 legislation enacting the Secure Choice Retirement Savings Program (SCRSP) for private sector workers whose employers do not offer a retirement plan. The legislation requires employers with five or more employees that do not offer specified retirement plans to put a payroll arrangement into place that requires employees to contribute a portion of their salary or wages to a retirement savings plan in the SCRSP, unless they opt out. Employers that already offer a qualified retirement savings program will not be mandated to have their employees enrolled in the SCRSP. Employers retain the right at all times to set up and offer their own qualified retirement plan. Registration Opens July 2019 According to the CalSavers website, employers will be able to start registering on July 1, 2019. Compliance will be phased in over a three-year period based on the size of the employer. It is intended that employers’ responsibility is simply as a pass-through, to deduct and submit contributions from employee wages. The program will be funded by an automatic 5% payroll deduction, the default contribution determined by the Secure Choice Investment Board. Employers will be required to automatically deduct contributions from employee paychecks and to transmit payroll contributions to the program. The employer makes no contribution into the retirement account. Employer Registration Deadlines Deadlines for registering for the CalSavers program are as follows:

|

|

Copyright © 2024 West Ventura County Business Alliance. All Rights Reserved.

1901 Solar Drive, Suite 105 | Oxnard, CA 93036 Phone: (805) 738-9100 | info@wvcba.org Site Map |